Buying your first property in India can feel overwhelming, but breaking it down into clear steps makes the process manageable. This complete guide is designed for first-time property buyers who want to make informed decisions and avoid costly mistakes when entering the Indian real estate market.

You’ll learn how to assess your financial readiness and understand different property types available across India. We’ll walk through the essential legal documentation and property verification steps that protect your investment, plus guide you through the home loan application process from start to finish.

We’ll also cover how to choose the right location, evaluate property value accurately, and conduct thorough property inspection and due diligence before making your purchase. By the end, you’ll have a solid home-buying checklist and the confidence to negotiate your first real estate investment transaction successfully.

Assess Your Financial Readiness Before Property Purchase

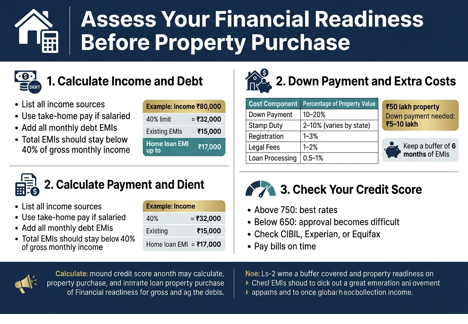

Calculate your total income and existing debt obligations

Getting a clear picture of your finances is the first step in your property buying journey. Start by documenting all your income sources – your salary, freelance work, rental income, or any other regular earnings. If you’re salaried, your take-home pay after taxes and deductions gives you the real number to work with.

Next, list all your monthly debt payments. This includes credit card EMIs, personal loans, car loans, education loans, and any other recurring financial obligations. Banks typically follow the 40% rule – your total EMIs (including the new home loan) shouldn’t exceed 40% of your gross monthly income.

For example, if your monthly income is ₹80,000, your total EMI burden should stay below ₹32,000. If you already pay ₹15,000 in existing EMIs, you can take on a home loan with a maximum EMI of ₹17,000.

Determine your down payment capacity and savings requirements

Most banks require a down payment of 10-20% of the property value. For a ₹50 lakh property, you’ll need ₹5-10 lakh upfront. But don’t stop there – factor in additional costs that catch many first-time property buyer guides in India seekers off guard.

Registration charges typically run 5-7% of the property value, stamp duty varies by state (2-10%), and legal fees add another 1-2%. Home loan processing fees, property insurance, and moving costs pile on more expenses.

| Cost Component | Percentage of Property Value |

| Down Payment | 10-20% |

| Stamp Duty | 2-10% (varies by state) |

| Registration | 1-3% |

| Legal Fees | 1-2% |

| Loan Processing | 0.5-1% |

Build a buffer of at least 6 months of EMIs in your savings account. This safety net protects you if income drops or unexpected expenses arise.

Check your credit score and improve it if necessary

Your credit score directly impacts your loan approval and interest rates. A score above 750 gets you the best rates, while scores below 650 make approval difficult. Check your score for free on platforms like CIBIL, Experian, or Equifax.

If your score needs work, focus on paying all bills on time, reducing credit card balances below 30% of limits, and avoiding new credit applications. Pay off smaller loans completely and keep old credit accounts open to maintain credit history length. Even small improvements can save thousands in interest over your loan term.

Understand tax implications and available deductions

Buying property in India for the first time comes with several tax benefits that reduce your overall cost. Under Section 80C, you can claim up to ₹1.5 lakh deduction on principal repayment. Section 24(b) allows a ₹2 lakh deduction on interest payments for self-occupied properties.

If you’re buying an under-construction property, you can’t claim interest deductions until possession, but you get a lump sum benefit for the entire construction period once you move in. Keep all payment receipts, bank statements, and legal documents organized for tax filing.

Registration and stamp duty payments also qualify for deductions under Section 80C in the year of purchase, reducing your immediate tax burden.

Understand Different Types of Properties Available

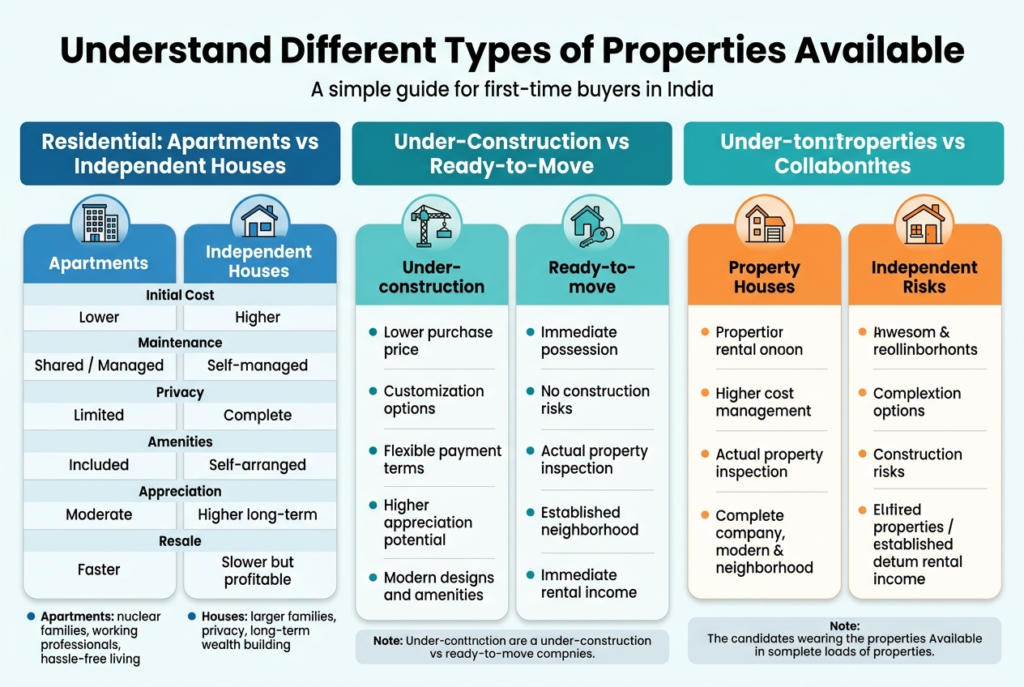

Compare residential apartments vs independent houses

When buying property in India first time, choosing between an apartment and an independent house affects your lifestyle, budget, and future investment returns. Apartments typically cost less upfront and offer modern amenities like security, parking, and recreational facilities. Most new developments include gyms, swimming pools, and landscaped gardens that would be expensive to maintain in a standalone house.

Independent houses give you complete control over your space, allowing renovations, extensions, and garden customization. You won’t deal with monthly maintenance fees, society rules, or neighbor noise issues. However, houses usually require higher initial investment and ongoing maintenance costs for security systems, water pumps, and structural upkeep.

| Feature | Apartments | Independent Houses |

| Initial Cost | Lower | Higher |

| Maintenance | Shared/Managed | Self-managed |

| Privacy | Limited | Complete |

| Amenities | Included | Self-arranged |

| Appreciation | Moderate | Higher long-term |

| Resale | Faster | Slower but profitable |

Apartments work well for nuclear families, working professionals, and those preferring hassle-free living. Houses suit larger families, people wanting privacy, or buyers planning long-term wealth building through real estate investment in India. Beginners often find it rewarding.

Explore under-construction vs ready-to-move properties

Under-construction properties offer significant cost advantages, with developers providing attractive payment plans and prices 15-30% lower than ready units. You can customize interiors, choose fixtures, and benefit from potential appreciation during construction. Many builders offer possession-linked payment schedules, reducing immediate financial burden.

Ready-to-move properties eliminate waiting periods and construction delays. You can inspect the actual unit, check build quality, and move in immediately after purchase. This option works perfectly for urgent housing needs or rental income requirements.

Under-construction advantages:

- Lower purchase price

- Customization options

- Flexible payment terms

- Higher appreciation potential

- Modern designs and amenities

Ready-to-move benefits:

- Immediate possession

- No construction risks

- Actual property inspection

- Established neighborhood

- Immediate rental income

Construction projects sometimes face delays due to approvals, funding issues, or legal complications. Ready properties might have hidden defects or outdated designs. Your property documentation in India process becomes more complex with under-construction units, requiring additional builder agreements and construction milestone tracking.

Consider your timeline, risk tolerance, and financial situation. First-time buyers often prefer ready properties for their predictability, while investors might choose under-construction options for better returns.

Evaluate commercial and investment property options

Commercial properties generate higher rental yields than residential units, typically offering 6-12% annual returns compared to residential properties’ 2-4%. Office spaces, retail shops, and warehouses attract business tenants willing to pay premium rents for prime locations.

Investment properties require different evaluation criteria than personal homes. Focus on rental potential, location growth prospects, and tenant demand rather than personal preferences. Areas near IT hubs, business districts, and transportation corridors usually offer better investment returns.

Commercial property types:

- Office spaces in business districts

- Retail shops in commercial complexes

- Warehouses in industrial areas

- Serviced apartments for corporate housing

- Co-working spaces in urban centers

Investment considerations:

- Rental yield calculations

- Maintenance and vacancy costs

- Tenant profile and lease terms

- Location appreciation potential

- Exit strategy planning

Commercial properties need a higher initial investment and may face longer vacancy periods. Tenant agreements involve complex lease terms, and property management requires business understanding. Some commercial projects offer assured returns for initial years, though these arrangements need careful legal verification.

Mixed-use developments combining residential and commercial spaces offer balanced investment opportunities. You can live in one unit while renting others, creating passive income streams while building equity. This approach works well for first-time property buyer guide India recommendations, especially for buyers seeking both residence and investment benefits.

Research local rental markets, vacancy rates, and upcoming infrastructure projects affecting property values. Commercial real estate often appreciates faster in developing areas, but requires patience and market knowledge.

Navigate Legal Documentation and Property Verification

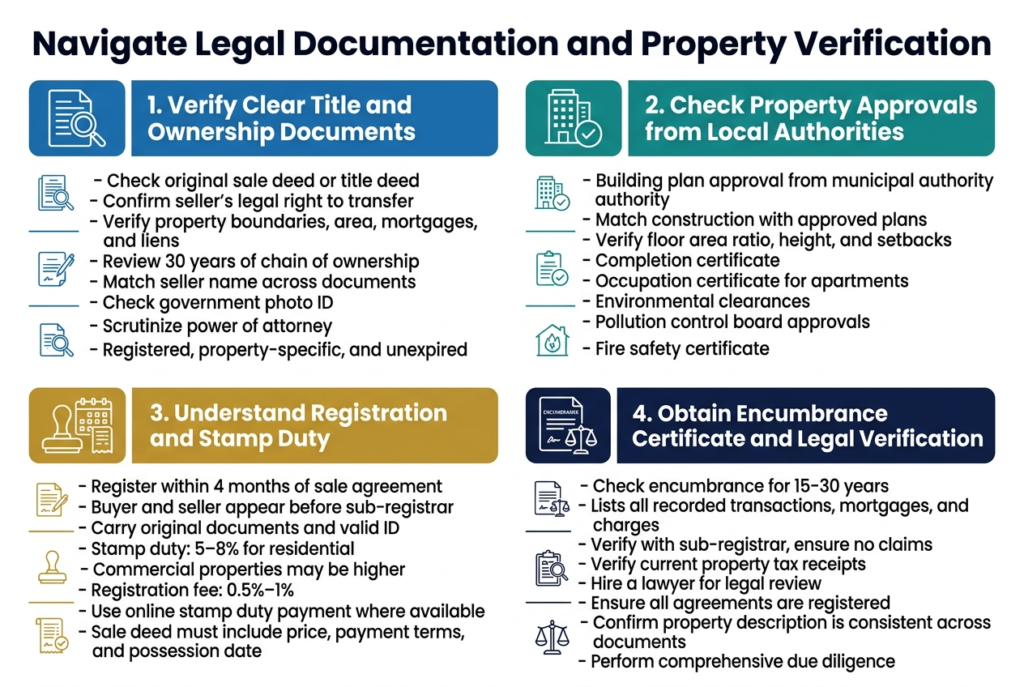

Verify Clear Title and Ownership Documents

Property verification in India requires meticulous attention to the title deed, which serves as proof of ownership. Start by examining the original sale deed or title deed to confirm the seller’s legal right to transfer the property. The document should clearly mention the property boundaries, area measurements, and any existing mortgages or liens.

Check the chain of ownership by reviewing all previous sale deeds dating back at least 30 years. This helps identify any gaps or irregularities in the ownership transfer. Look for the seller’s name consistency across all documents and verify their identity through government-issued photo identification.

Power of attorney documents need special scrutiny. If the seller is acting through a representative, ensure the power of attorney is registered, specific to the property, and hasn’t expired. General power of attorney documents often lack legal validity for property transactions.

Check Property Approvals from Local Authorities

Local authority approvals form the backbone of legitimate property ownership in India. Begin by verifying the building plan approval from the municipal corporation or local development authority. The construction should match the approved plans exactly, including floor area ratios, building height, and setback requirements.

Obtain copies of the completion certificate, which confirms the building meets all safety and construction standards. For apartment complexes, check the occupation certificate that permits residents to occupy the building legally.

Environmental clearances are mandatory for projects exceeding certain size limits. Verify pollution control board approvals and ensure the builder has obtained all necessary environmental permits. Fire safety certificates from the fire department are equally important, especially for high-rise buildings.

Understand Registration Process and Stamp Duty Requirements

Property documentation in India involves understanding the registration process that makes your property purchase legally binding. Property registration must occur within four months of executing the sale agreement. Both buyer and seller need to appear before the sub-registrar with original documents and valid identification.

Stamp duty rates vary across states and property types. Residential properties typically attract 5-8% stamp duty, while commercial properties may face higher rates. Some states offer reduced stamp duty rates for women buyers or first-time property buyer guides in India participants.

Registration fees usually range from 0.5% to 1% of the property value. Calculate these costs beforehand and factor them into your budget. Many states now offer online payment options for stamp duty, making the process more convenient.

Document preparation requires precision. The sale deed should include an accurate property description, agreed purchase price, payment terms, and the possession date. Any modifications after signing may require additional stamp duty payments.

Obtain Legal Clearance and Encumbrance Certificate

The encumbrance certificate provides a complete transaction history of the property for a specified period. Request an encumbrance certificate covering at least 15-20 years to understand all past transactions, mortgages, and legal proceedings involving the property.

Legal clearance involves verifying that the property is free from disputes, litigation, or pending court cases. Check with local civil courts and revenue departments for any ongoing legal proceedings. Properties under litigation cannot be sold until disputes are resolved.

Tax clearance certificates confirm all property taxes, municipal taxes, and utility bills are paid up to date. Outstanding dues often transfer to the new owner, creating unexpected financial burdens.

Survey settlement records help verify the actual property boundaries and area. Compare these government records with the property documents to identify any discrepancies. Boundary disputes are common sources of future legal complications that proper verification can prevent.

Master Home Loan Application and Approval Process

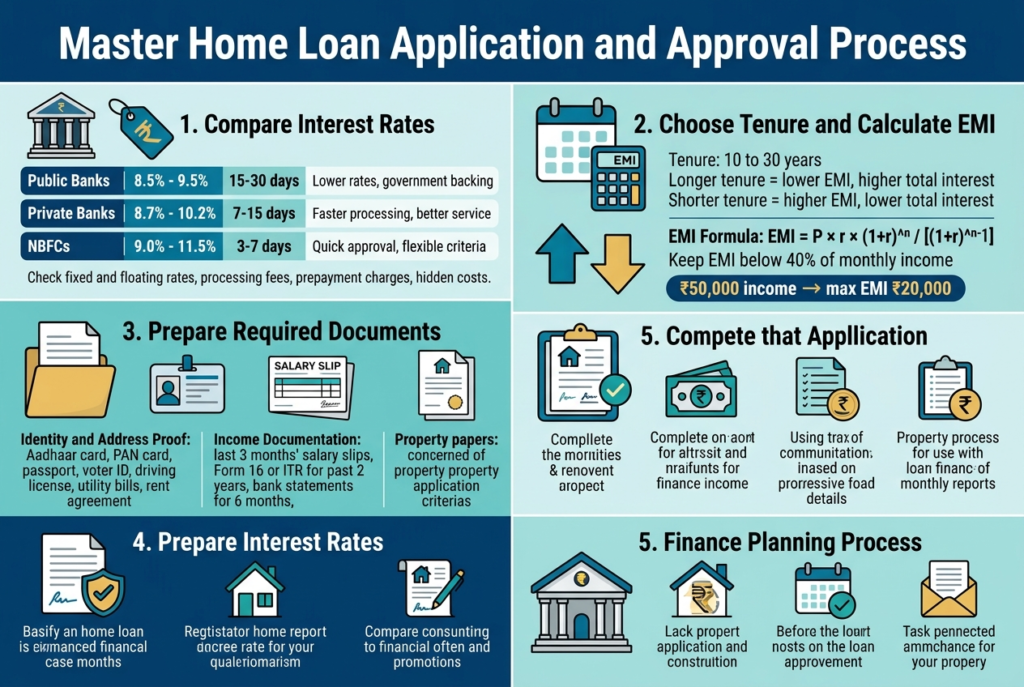

Compare interest rates across different banks and NBFCs

Home loan interest rates can make or break your home loan application process in India experience. Banks typically offer rates between 8.5% to 11.5%, while NBFCs might charge slightly higher but provide faster processing. State Bank of India, HDFC Bank, ICICI Bank, and Axis Bank are popular choices for first-time property buyer guides in India seekers.

Check both fixed and floating rates. Fixed rates stay the same throughout your loan tenure, while floating rates change with market conditions. Most first-time buyers prefer floating rates as they’re usually lower initially. Compare processing fees, prepayment charges, and hidden costs alongside interest rates.

| Lender Type | Interest Rate Range | Processing Time | Key Benefits |

| Public Banks | 8.5% – 9.5% | 15-30 days | Lower rates, government backing |

| Private Banks | 8.7% – 10.2% | 7-15 days | Faster processing, better service |

| NBFCs | 9.0% – 11.5% | 3-7 days | Quick approval, flexible criteria |

Understand loan tenure options and EMI calculations

Loan tenure directly impacts your monthly budget when buying a property in India for the first time. Choose between 10 to 30 years based on your age and income. Longer tenure means lower EMIs but higher total interest. Shorter tenure increases the monthly burden but saves money long-term.

Calculate your EMI using the formula: EMI = P × r × (1+r)^n / [(1+r)^n-1], where P is the principal, r is the monthly interest rate, and n is the tenure in months. Most banks offer online EMI calculators for quick estimates.

Keep your EMI below 40% of your monthly income. If you earn ₹50,000 monthly, your EMI shouldn’t exceed ₹20,000. This leaves room for other expenses and emergencies. Consider salary growth potential when choosing tenure.

Prepare the required documents for the loan application

Documentation is crucial for your home loan application process in India success. Banks need proof of identity, income, employment, and property details. Gather these documents early to avoid delays.

Identity and Address Proof:

- Aadhaar card, PAN card, passport

- Voter ID, driving license

- Utility bills, rent agreement

Income Documentation:

- Last 3 months’ salary slips

- Form 16 or ITR for the past 2 years

- Bank statements for 6 months

- Employment certificate

Property Documents:

- Sale agreement copy

- Property title documents

- Approved building plans

- NOC from builder/society

Self-employed applicants need additional documents like business registration, profit-loss statements, and GST returns. Keep both the original and photocopies ready.

Navigate loan approval and disbursement procedures

Banks follow a structured approval process that takes 7-30 days, depending on the lender. After document submission, they verify your income, employment, and credit score. A CIBIL score above 750 ensures faster approval and better rates.

The bank conducts technical and legal verification of the property. Technical evaluation checks construction quality, while legal verification ensures a clear title. Both reports must be satisfactory for loan approval.

Once approved, you’ll receive a sanction letter mentioning the loan amount, interest rate, and terms. Read this carefully before signing. Disbursement happens in stages – typically 20% on agreement signing, 60% during construction, and 20% on completion.

Track your application status online or through customer service. Most banks provide regular updates via SMS and email.

Learn about government schemes for first-time buyers

Government schemes significantly reduce the financial burden for first-time property buyers in India followers. Pradhan Mantri Awas Yojana (PMAY) offers interest subsidies up to ₹2.67 lakh for eligible buyers. This scheme covers different income groups with varying subsidy amounts.

PMAY Benefits by Income Group:

- EWS/LIG: Up to ₹2.67 lakh subsidy

- MIG-I: Up to ₹2.35 lakh subsidy

- MIG-II: Up to ₹2.30 lakh subsidy

Credit-Linked Subsidy Scheme (CLSS) under PMAY provides interest subsidies on home loans. The subsidy gets credited directly to your loan account, reducing the principal amount.

State governments offer additional schemes. Delhi has its own housing scheme, while Maharashtra provides stamp duty rebates for women buyers. Research local schemes in your city before applying for loans.

Some banks partner with government schemes to offer special interest rates. Check if your chosen lender participates in these programs to maximize benefits.

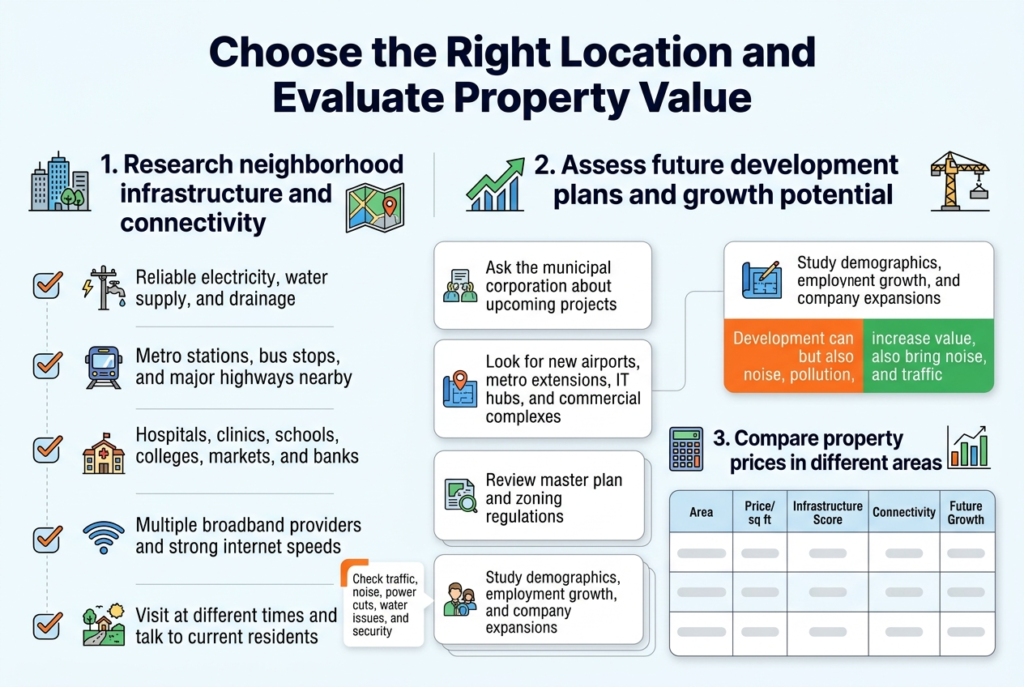

Choose the Right Location and Evaluate Property Value

Research neighborhood infrastructure and connectivity

When you’re buying a property in India for the first time, picking the right neighborhood makes all the difference. Start by checking what’s already there and what’s coming soon. Look for basic infrastructure like reliable electricity, water supply, and proper drainage systems. These might sound boring, but they’ll save you countless headaches later.

Transportation links are your lifeline to the rest of the city. Check how close you are to metro stations, bus stops, and major highways. A well-connected area might cost more upfront, but you’ll save time and money on daily commutes. Don’t just look at current options – check if new metro lines or highways are planned for your area.

Healthcare and education facilities nearby add serious value to your investment. Hospitals, clinics, good schools, and colleges make life easier and boost property prices over time. Shopping centers, banks, and markets within walking distance or a short drive make daily life smoother.

Internet connectivity deserves special attention, especially if you work from home. Check if multiple broadband providers service the area and what speeds they offer. Poor internet can be a deal-breaker in today’s world.

Visit the area at different times – morning rush hour, afternoon, and evening. This gives you a real feel for traffic patterns, noise levels, and general activity. Talk to current residents if possible. They’ll give you honest insights about power cuts, water issues, or security concerns that you won’t find in any brochure.

Assess future development plans and growth potential

Smart property buyers look beyond what exists today. Future development plans can dramatically increase your property’s value or, if you’re unlucky, create problems you never saw coming. Start by checking with local municipal corporations about upcoming projects in your target area.

Major infrastructure projects like new airports, metro extensions, IT hubs, or commercial complexes can transform an area completely. Properties near these developments often see significant price appreciation. Look for government announcements about smart city initiatives, industrial corridors, or special economic zones.

But development can be a double-edged sword. A new highway might improve connectivity, but also bring noise and pollution. A shopping mall nearby sounds great until you realize it means constant traffic and parking issues. Always consider both the benefits and potential downsides.

Check the area’s master plan and zoning regulations. These documents show what kind of development is allowed and where. You don’t want to buy a peaceful residential property only to find out a commercial complex can legally come up right next door.

Real estate investment in India for beginners should also look at demographic trends. Areas attracting young professionals or families often see sustained growth. Check employment opportunities in the region, especially if major companies are setting up offices nearby.

Compare property prices in different areas

Price comparison isn’t just about finding the cheapest option – it’s about understanding value. Create a simple spreadsheet comparing properties across different neighborhoods, factoring in size, age, amenities, and location advantages.

Start with price per square foot as your baseline metric. But remember, a Rs. 3,000 per square foot property in a well-developed area might be a better value than a Rs. 2,500 property in an area with poor infrastructure. Factor in additional costs you’ll face in less developed areas – backup power solutions, water tankers, or longer commute costs.

| Area | Price/sq ft | Infrastructure Score | Connectivity | Future Growth |

| Central Location | ₹8,000 | 9/10 | Excellent | Moderate |

| Emerging Suburb | ₹4,500 | 6/10 | Good | High |

| Outer Ring | ₹3,200 | 4/10 | Fair | Very High |

Look at recent sales data, not just listing prices. Websites like MagicBricks and Housing.com show market trends, but also check with local brokers for ground reality. They know about recent transactions that might not be publicly listed.

Consider rental yields if you’re thinking about investment potential. Calculate annual rental income as a percentage of property cost. Areas with good rental demand often indicate strong fundamentals.

Don’t forget about resale potential. Properties in established areas with good schools, hospitals, and transportation typically hold their value better. While emerging areas might offer higher growth potential, they also carry more risk. Balance your risk appetite with your investment timeline when making this crucial decision.

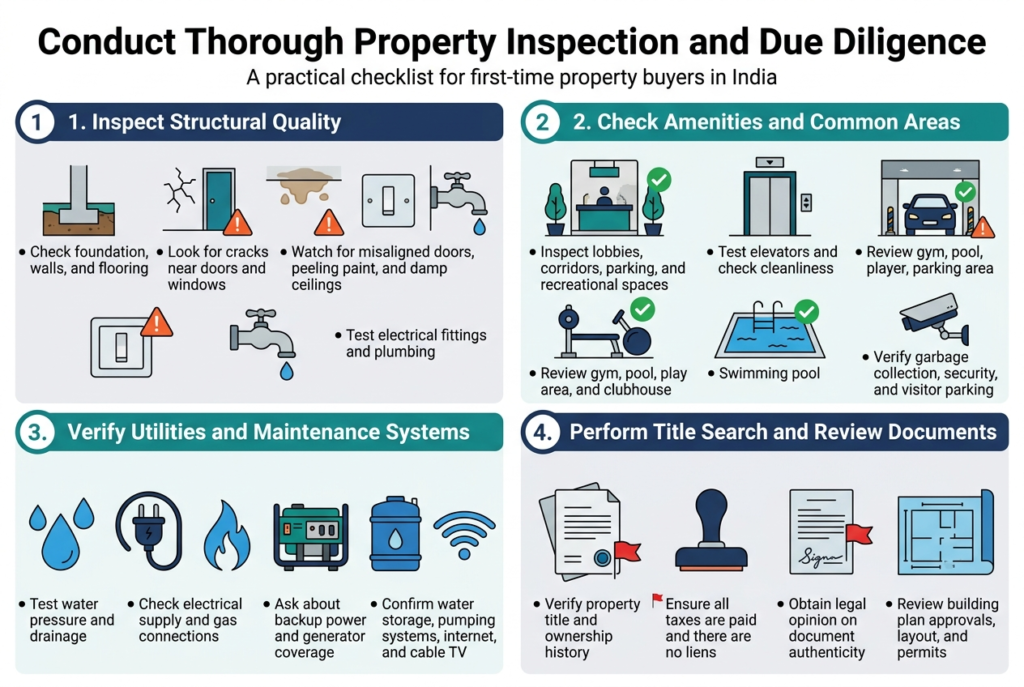

Conduct Thorough Property Inspection and Due Diligence

Inspect structural quality and construction standards

Start with the foundation and work your way up. Look for cracks in walls, especially around doors and windows – these often signal structural issues. Pay attention to the quality of materials used. Are the tiles properly aligned? Do the walls feel solid when you tap them? Poor construction shows up in uneven flooring, misaligned doors that don’t close properly, and paint that’s already peeling.

Check the ceiling for water stains or dampness marks. These red flags indicate potential leakage problems that could cost you thousands later. Test the electrical fittings by switching lights on and off. Examine the plumbing by running water in all taps and flushing toilets to ensure proper water pressure and drainage.

For property inspection tips India, bring a checklist and take photos of any concerns. Don’t rely on your memory alone. If you notice significant structural issues, consider hiring a professional inspector before making your final decision.

Check amenities and common area facilities

Walk through all common areas including lobbies, corridors, parking spaces, and recreational facilities. These spaces reflect how well the property is managed and maintained. Check if elevators work smoothly and if the lobby appears clean and well-lit.

Visit the gym, swimming pool, children’s play area, and clubhouse if available. Test equipment where possible and observe the cleanliness standards. Well-maintained amenities add value to your investment and improve your living experience.

Don’t forget practical amenities like garbage collection areas, security systems, and visitor parking. These day-to-day conveniences matter more than you might initially think. A property with poor common area maintenance often indicates future problems with overall management.

Verify utility connections and maintenance systems

Test all utility connections personally. Turn on water taps in multiple locations to check pressure and quality. Switch on electrical appliances to ensure an adequate power supply without fluctuations. If the property has gas connections, verify they’re properly installed and functional.

Ask about backup power systems, especially in areas with frequent electricity cuts. Check if the building has a generator and whether it covers common areas and individual apartments. Water storage and pumping systems need attention too – find out about water sources and storage capacity.

Inquire about internet and cable TV connectivity. Many modern buyers consider high-speed internet essential, so verify which service providers operate in the area and their reliability. These utility checks form a crucial part of real estate due diligence in India for first-time buyers.

Review the builder’s reputation and track record

Research the builder’s history before signing anything. Look up their previous projects and visit completed developments if possible. Talk to residents in these projects about their experiences with construction quality, timely delivery, and after-sales service.

Check online reviews and real estate forums for feedback about the builder. Social media groups and local community pages often contain honest opinions from actual buyers. Look for patterns in complaints – are there recurring issues with delayed possession, poor construction quality, or unresponsive customer service?

Verify the builder’s financial stability and legal standing. A reputable builder should have proper licenses, good credit ratings, and no major legal disputes. This research protects your investment and ensures a smoother property ownership experience as a first-time property buyer guide India recommends.

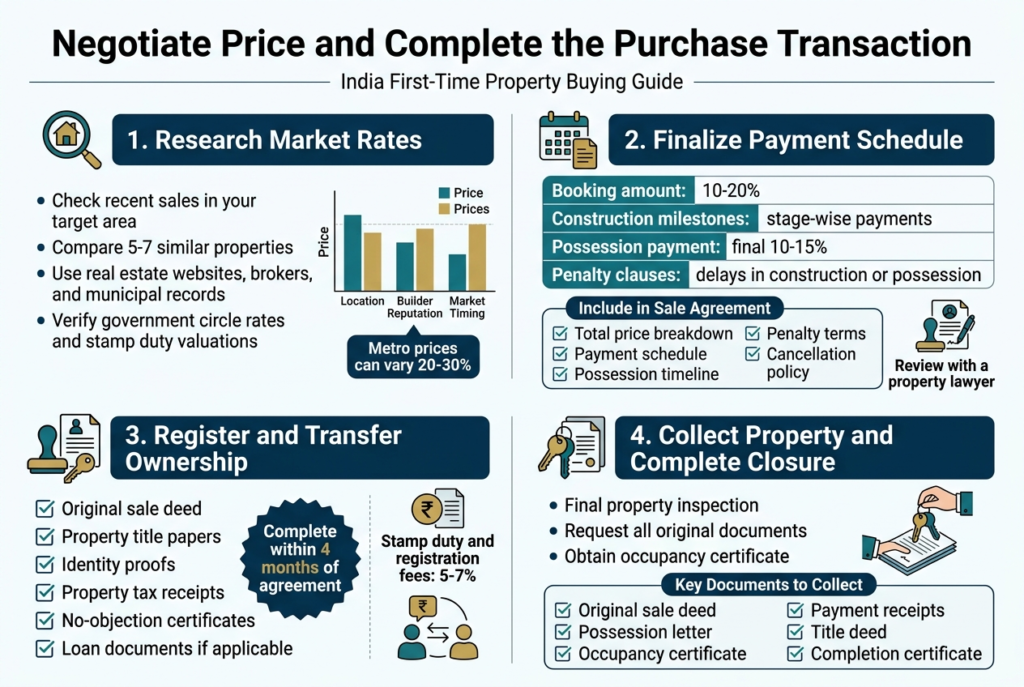

Negotiate Price and Complete the Purchase Transaction

Research market rates for effective price negotiation

Understanding current market rates gives you serious leverage when buying property in India for the first time. Start by checking recent sales in your target area through real estate websites, local brokers, and municipal records. Look for properties similar in size, age, and amenities to get accurate comparisons.

Property rates vary dramatically based on location, builder reputation, and market timing. In metro cities, prices can differ by 20-30% between similar properties just a few kilometers apart. Create a comparison chart with at least 5-7 comparable properties to establish a realistic price range.

Connect with multiple real estate agents and ask for their market analysis. Each agent brings different insights about recent transactions and upcoming projects that might affect pricing. Don’t rely on just one opinion – cross-reference information from various sources.

Check government circle rates and stamp duty valuations for your area. These official rates often lag behind market prices but provide a baseline for negotiations. Banks also use these rates for loan approvals, so understanding them helps during the home loan application process in India.

Finalize payment schedule and agreement terms

The payment structure significantly impacts your property purchase transaction in India experience. Most builders offer flexible payment plans linked to construction milestones, while resale properties typically require faster payment schedules.

For under-construction properties, negotiate payment terms that protect your interests:

- Booking amount: Usually 10-20% of the total cost

- Construction milestones: Payments tied to completed floors/stages

- Possession payment: Final 10-15% on receiving keys

- Penalty clauses: Include delays in construction or possession

Document every agreement detail in writing. The sale agreement should specify exact amounts, payment dates, and consequences for delays from either party. Include clauses covering:

| Agreement Component | Key Details |

| Total price breakdown | Base cost, taxes, additional charges |

| Payment schedule | Amounts and due dates |

| Possession timeline | Expected handover date |

| Penalty terms | For both buyer and seller delays |

| Cancellation policy | Refund terms and conditions |

Review all terms with a property lawyer before signing. This small investment prevents major legal complications later.

Complete registration and transfer of ownership

Property registration legally transfers ownership and protects your investment. The registration process involves multiple steps that must be completed within four months of the agreement date.

Gather all required documents before heading to the sub-registrar’s office:

- Original sale deed

- Property documents and title papers

- Identity proofs of all parties

- Property tax receipts

- No-objection certificates

- Loan documentation (if applicable)

Pay the required stamp duty and registration fees. These charges vary by state but typically range from 5-7% of the property value. Some states offer reduced rates for women buyers or first-time purchasers.

The registration appointment requires the presence of both buyer and seller with witnesses. Biometric verification and photograph requirements have made the process more secure but also more time-consuming. Book your slot well in advance to avoid delays.

After successful registration, you’ll receive the registered sale deed – your legal proof of ownership. Keep multiple copies in different safe locations.

Understand possession timelines and the handover process

Possession, marking the final step in your property purchase journey, requires careful planning and documentation. For ready-to-move properties, possession usually happens within 15-30 days of completing payments and registration.

Under-construction properties follow different timelines based on completion status. Builders typically provide 6-12 months’ notice before possession, allowing you to arrange final payments and home loans.

The handover process includes several important checks:

- Physical inspection: Verify all promised amenities and finishes

- Utility connections: Confirm electricity, water, and gas connections

- Common area access: Check elevators, parking, and shared facilities

- Defect documentation: List any construction issues for rectification

- Maintenance handover: Understand society rules and ongoing charges

Obtain these essential documents during possession:

- Occupation certificate

- Completion certificate

- Electricity and water connection papers

- Society formation documents

- Maintenance and utility guidelines

Plan your possession date strategically, considering loan disbursement schedules and moving arrangements. Many buyers face stress during this phase due to poor timing coordination.

Keep detailed records of all possession-related communications and documents. These serve as important references for warranty claims and future property transactions.

Getting your financial house in order and understanding what’s available in the market sets the foundation for a smart property purchase. The paperwork might seem overwhelming at first, but proper documentation and verification protect you from future headaches. Getting pre-approved for a home loan gives you a clear budget and strengthens your negotiating position when you find the right place.

Location research and property valuation help you make decisions that pay off in the long run. Don’t skip the inspection phase – it’s your chance to spot problems before they become your problems. Take your time during negotiations and remember that buying property is a marathon, not a sprint. Start with your finances, do your homework on every aspect, and you’ll find yourself holding the keys to your new home sooner than you think.